AppTech Payments Corp. is a Story Stock of Paid Promotions Without Any Operational Technology to Back it Up

· AppTech Payments Corp (APCX) does not have any developed products, their digital payment and banking platform are still in the development and beta stage. Their legacy business has never generated any significant revenues nor profits.

· APCX’s digital payments and banking platform might be worthless. Most of their intangible capitalized assets were impaired and were related to development of their fintech platform, “Commerse” in collaboration with Infinios through a strategic partnership that has been terminated.

· APCX’s new agreement with InstaCash, made in June 2023, is supposed to compete with Venmo, Zelle, and CashApp but is most likely worthless and won’t amount to anything in the future. InstaCash doesn’t even have an app yet.

· The company has no cash and urgently needs to raise it to keep its doors open.

· APCX paid over $500K to promoters in 2022 and kept paying for it in 2023 as well right before filing an 8K for an ATM Offering on 8/21/23.

AppTech Payments Corp. is a former OTC Pink Sheet traded payment processing company parading as a Fintech company that will compete with Zelle, Venmo, and Cash App. It has been around at least since 2013 and historically the company has not generated any meaningful revenues from their electronic payment processing and merchant services business. They have recently ended a partnership that appears to be accounting for most of their digital banking payment ambition business and impaired most of their intangible assets related to it. They need cash and have filed an 8K on 8/21/23 announcing an ATM to raise $18M right after the company started a paid promotion campaign in August.

A Fintech Story in the Making that Might no Longer Exist

APCX was formerly known as Transcendent One, Inc. In 2013, Transcendent, an electronic transaction processing and merchant services company, merged with AppTech Corp.

At the time of the merger, on 5/13/13, the current CEO of APXC, Luke D’Angelo, stated in a PR:

"Our company is very excited about our continued growth in the financial services and technology spaces. We believe our subsequent business developments, joint ventures, and entry into the public market will provide access to gaining considerable market share in the near future,"

On the contrary to D’Angelo’s above statement, since the merger and public access to financial markets APCX has failed to generate any meaningful revenues and racked up $154M in accumulated deficit, as shown below:

Source: APCX 10Ks

By 2021 APCX rebranded itself as a digital financial services company that will offer corporations, small and midsize enterprises and consumers innovative payment processing, reconciliation, and digital banking technologies from electronic payment processer and merchant services company. They managed to uplist from the OTC pink sheets to the NASDAQ in 2022. As of the date of their last financial statements, the technology is not operational but still in development and started to be beta tested at the end of 2022.

It appears that they might not be able to deliver the technology at all since they licensed their intellectual property for digital banking technology from Infinios Financial Services BSC (former NEC Payments B.S.C.) that is based in Bahrain and is in the business of digital banking and payment technology. Under the strategic partnership agreement APCX issued 1.8M shares in 2020 absurdly valuing this partnership at $68M while booking $3.8m in assets for it and the rest as an expense, substantially increasing accumulated deficit from $45M in 2020 to $124M by 2021. The transaction has not generated any developed product to this day.

From APCX Q223 report:

“AppTech is developing an embedded, highly secure digital payments and banking platform that powers commerce experiences for clients and their customers. Based upon industry standards for payment and banking protocols, we will offer standalone products and fully integrated solutions that deliver innovative, unparalleled payments, banking, and financial services experiences.”

As of Q223, APXC announced in their financial statements that the partnership has been terminated and Infinios turned off all of their services to APCX forcing them to impair $6M worth of intangible capitalized assets related to it.

Assets impaired related to the Infinios partnership termination accounted for most of APCX’s intangible capitalized assets leaving them with just $1.3M worth of capitalized software development and license assts.

This leads to a reasonable question, what is their proprietary fintech platform, Commerse, worth right now? The software was developed with Infinios, Infinios turned off their services and APCX wrote down most of its capitalized software development cost related to this partnership and the Commerse platform.

Does Commerse platform even operational without Infinios services and digital banking intellectual property?

New Worthless Partnership

In June 2023, APCX entered into a Strategic Partnership Agreement with InstaCash to develop mobile-to-mobile contactless payment system with digital banking services to add to their Commerse platform capabilities, a cloud-based fintech platform that is still in development stage and now under a big question mark since the strategic partnership with Infinios Financial Services was terminated.

The agreement will allow InstaCash to license all the APCX intellectual property and APCX will help them build the product and take an equity stake. It is the story on repeat, a licensing deal for both companies to collaborate to build a full service digital financial service and banking platform backed up by APCX intellectual property portfolio. The only difference is that in the InstaCash agreement, APCX is taking a stake in it whereas Infinios Financial Services took a stake in APCX significantly overvaluing the deal. Meanwhile, InsatCash has no developed product or app, and neither does APCX.

The tiny revenue that APCX had generated so far relates to their old business of electronic payment processing and merchant services business, not from digital payments and banking platform.

CEO Luke D’Angelo is quoted from the InstaCash Agreement PR:

“The agreement will allow us to demonstrate the core differentiation of our Fintech platform, Commerse™. This platform is a patent-backed, modular, cloud-based solution with industry-leading security features. We look forward to working with the InstaCash team and our network of banking partners to develop and manage the platform,”

And here are his comments at the time of the Infinios Strategic Agreement PR on 10/5/20:

“Our significant equity and cash investment into the partnership with NECP provides AppTech with the clearest and quickest opportunity to bring to market cutting edge technologies and achieve scale and profitability from their rapid adoption.”

He mentions “rapid adoption” of something that two years later is not even a developed product.

Now, InstaCash, Inc. does not even look like a real company that has any potential to compete with likes as Zell, Venmo, or Cash App, as they claim on lower transfer fee and better security protocol. A seven-year-old could have made their website, shown below:

Source: https://instacash.cash

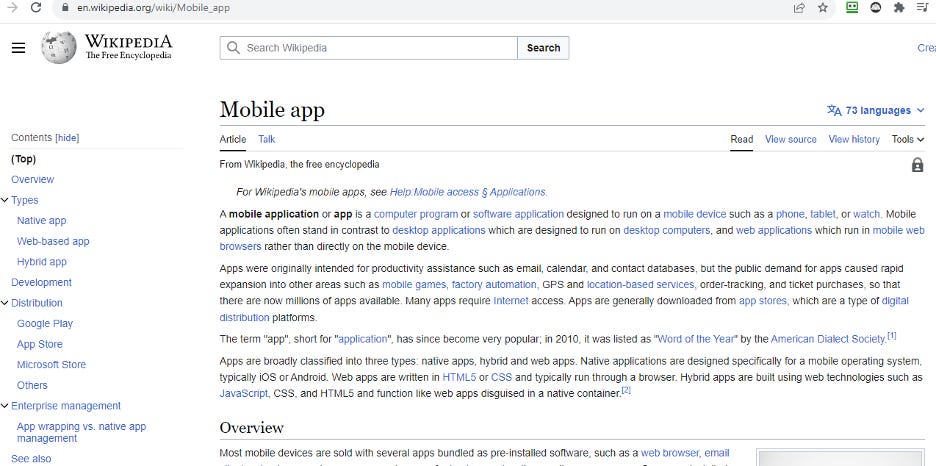

It is a two-pager website! And this is the company that will apparently be directly competing with Venmo, Zelle, and Cash App. They don’t even have an app yet. When you click on the mobile phone app link, it laughably goes to a Wikipedia page, as shown below:

APCX is left with $749K in cash while burning $9M per quarter which explains managements aggressive paid promotions campaign that started in August followed by an 8K filing announcing that they entered into an ATM agreement to raise $18M.

When the Product Does Not Exist Just Pay Promoters to Tell a Story

August was a busy month for APCX, with a series of promotional interviews, starting with a PR at the end of July and then another PR at the beginning of August, stating that APCX will make a guest appearance with New to The Street TV, syndicate televised outlets of Newsmax, Fox Business Network , and Bloomberg TV. For an outsider that looks like legitimate exposure by respected financial news channels, what the PR is not saying is that APCX paid New to The Street to cover them since New to The Street is a paid advertiser.

New to the Street’s disclaimer:

Source: https://www.newtothestreet.com/disclosures

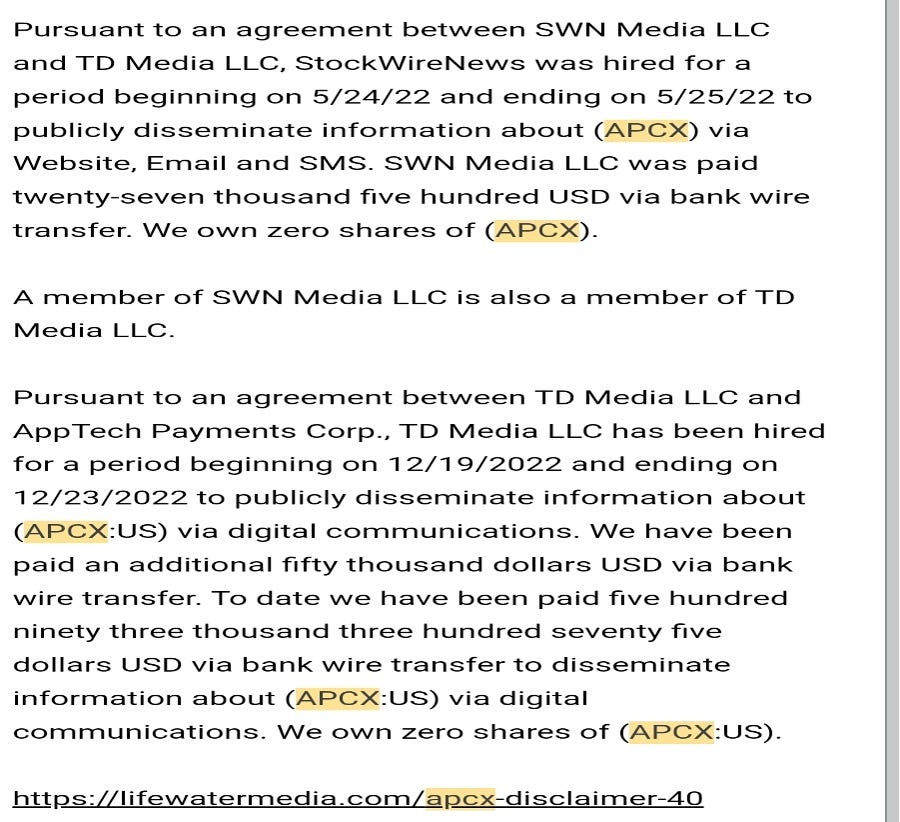

APCX engaged another promoter that they used since December 2022, Investorideas.com right into filing their $18M ATM offering.

Source: https://www.investorideas.com/About/Disclaimer.asp

APCX has engaged them as far back as December 2022 and since then Investorideas.com has published numerous articles on APCX.

Source: https://www.investorideas.com/About/News/Clientspecifics.asp

In 2022 APCX paid $50K to promote through Fierce Investor promotional emails, in addition to already paying $593K for Fierce Investor’s services. APCX is a company that has not generated any return to their shareholders supporting its operations by consistently raising cash in public markets but has the audacity to spend more than half a million dollars on paid promotions, more than the revenue that they have generated since at least 2017, instead of using investors’ money to invest in their business and actually develop a product that have been promised since at least 2021.

Conclusion

My price target for APCX is $0. I believe APCX is a story stock and a scam. They don’t have any developed product, or app, for digital banking technology and will most likely never come to be anything anytime soon but a promotional talking point for insiders and paid promoters to raise more and more cash from unaware investors as they have done since at least 2013 and no growth came out of it. And even if they do manage to commercialize whatever they currently have, which is not much, since they are no longer in partnership with Infinios that accounted for most of their intangible capitalized assets related to digital banking technology and InstaCash App does not have any developed and working product either while promoting this deal as direct competitors with Zelle, Venmo, and Cash App, which are growing fast and have more financial resources and market share to capture any new development in Fintech industry. Plus, InstaCash should first learn how to make a professional website before attempting to compete with the majors in the digital banking market.

Disclosure:

I am/we are holding short position in APCX.

By viewing material in this article you agree to the following Terms. You agree that use of AVResearch is at your own risk. In no event will you hold AVResearch or any affiliated party liable for any direct or indirect trading losses caused by any information in this report. You further agree to do your own research and due diligence before making any investment decision with respect to securities covered herein. You represent to AVResearch that you have sufficient investment sophistication to critically assess the information, analysis and opinion in this report. You further agree that you will not communicate the contents of this report to any other person unless that person has agreed to be bound by these same terms of service.

My name is Mehrak (Mayrack) Hamzeh, I am the author of the patents for AppTech, acting as CTO and Director of IP and Partnerships. Please contact me directly at mhamzeh@apptechcorp.com so you can get the real scoop versus making up defamatory comments. Your short position needs to run for the hills. We are a real deal, get your facts straight, InstaCash is a real deal, please check their website by Friday their new logo/brand will be up. For anyone doubters out there, call me 858.997.9135.

And quickly working up a short report after they just announce an acquisition… goes to show